With all of the articles in the media these days about rising real estate prices and the unaffordability of homes, you would be forgiven in thinking that buying a house or condo is all bad news.

As any of you who have recently purchased a home or refinanced a home knows, there is in fact some very good news. So good in fact, that when I looked into it for the first time, I said to myself, that can’t be right.

Let’s start with the bad news.Yes, real estate is more expensive. When I was growing up, a million dollar home brought to mind a mansion with manicured grounds, an indoor pool and a butler. Contrast that to today, when I can show you a fixer upper in a decent neighbourhood in Toronto, that will cost over a million.

No question, you pay more now, than you used to pay.

But does it cost you more? A key factor influencing the rise in real estate prices is the lowering of mortgage rates.

You see, with a few rare exceptions, we don’t buy real estate out right. We put down a deposit, typically in the 5% to 20% range and borrow the rest. That 80% to 95% of the cost of the home is borrowed, and borrowing right now is cheap.

Really cheap.

A few years back I qualified as a mortgage broker so that I could add value to my realtor clients. As a result, on a daily basis I receive updates from lenders on the rates they are offering. Right now (May 28, 2014), there are a number of lenders offering 5 year fixed mortgages, with a 25 year amortization period, at 2.99%.

This is the first piece of very good news.

A mortgage rate of 2.99% means that for every $100,000 you borrow, the monthly cost is $472.73. I had to check this twice as it seemed crazy to me that you could finance a house of $425,000 for under $2,000 per month.

You still need to qualify for the mortgage and of course you need to be prepared for the likelihood of a higher rate when you renew in 5 years, but make no mistake, when you are ready to buy a home, low interest rates are amazing.

As any of you who have bought a home in a multiple offer scenario know, less than $500 per month for $100K is very reassuring when you have to stretch your budget to get the home of your dreams.

Here is the second piece of very good news.

With a lower mortgage rate, not only is your payment lower, the amount of your payment that goes to principal is higher.

That monthly cost of $472.73 per $100K I mentioned? From your very first payment, you are paying almost as much principal as you are interest. I couldn’t believe this as I recall how I used to see my mortgage summary from the lender each year showing that despite those massive monthly mortgage payments, only a small fraction went to paying down principal.

With current mortgage rates, the first payment of $472.73 is comprised of a principal payment of $225.10 and an interest payment of $247.63. From day one, your monthly mortgage payment is about 48% principal, and every subsequent mortgage payment is even better.

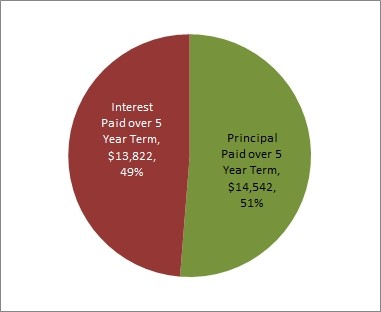

By the end of your five year term, more than half of what you paid towards your mortgage will have gone to reducing your principal!

$100,000 Loan at 2.99% on a Five Year Term (25 Year Amortization)

None of us like paying more than we used to but we can take comfort in the fact that for real estate, the low mortgage rates of today mean that financing that expensive home costs less than it used to and we pay down more of the principal, quicker!

None of us like paying more than we used to but we can take comfort in the fact that for real estate, the low mortgage rates of today mean that financing that expensive home costs less than it used to and we pay down more of the principal, quicker!

A number of my clients choose me as their Realtor because they appreciate my comfort and understanding with the financing aspects of their new home purchase.

If you or anyone you know are considering buying a home or an investment, please contact me to discuss your options. I would love to be responsible for what comes next.

Regards,

Jeff