One of the few constants in real estate recently has been the low levels of buyers, at least compared to the available number of properties.

The number of sales in Toronto that took place in 2025 was down about 8% from the level of transactions in 2024, which itself was lower than 2023 and so forth.

If we look at the level of sales that took place in Q4 2025 and Q1 2026, it’s down about 9% compared to the same time period a year ago (Q4 2024 and Q1 2025), so things are not getting better.

There’s a saying in real estate, which is “Sellers live in the past, buyers live in the future” and that seems to very much be the case now. We have sellers who are stubbornly holding onto what their home used to be worth and we have buyers who are shaking their heads and refusing to pay what the home is worth now, in the fear that the market will keep dropping.

What makes buyers hold off on making a purchase? That’s a complicated question, but there are three big factors that impact buying decisions on a macro level. Let’s get into them.

Numero Uno – The Cost of Borrowing

Only about 10% to 15% of purchasers in the GTA do so without borrowing money in the form of a mortgage. As such, the interest rates that are charged have a big impact on the carrying cost of the property.

Borrowers have the choice between a variable rate mortgage or a fixed rate mortgage and which is most popular does shift based on the perceived risk of rate changes over time, as well as how that risk is factored into the rates being offered by lenders.

In general, if there is uncertainty, borrowers tend to favour fixed rates, so they know how much it will cost them over the length of the term of their mortgage. As such, in the past year, we’ve seen more people shifting to fixed rate mortgages, as reported by CMHC in the 2025 Year-In-Review report. Variable mortgages likely make up about 40% of the pool of borrowers, with the remainder in fixed rate mortgages.

The variable rate that banks offer is directly impacted by the overnight rate charged by the Bank of Canada, which is effectively the rate as which banks can borrow from the BOC. In addition to the variable mortgage rate banks offer, the overnight rate also directly impacts HELOCs and other variable lending that uses the bank prime interest rate to determine the rate charged.

As we write this article in May, 2026, it has now been close to two years since the Bank of Canada started dropping the overnight rate. In July 2023, the rate was set at 5% and until June 2024, it remained there. From June 2024 onward until October 2025, we saw a cutting cycle, where rates dropped down from 5% to 2.25%.

Since October 2025, we’ve remained at that same 2.25% level. Our latest BOC of announcement on April 29, 2026 saw the overnight rate stay at 2.25%, which means it is the 4th announcement in a row with no change to the rate. Put another way, it’s been six months of no change to the cost of borrowing, at least on the variable interest rate side of the mortgage equation.

If we look at fixed mortgage rates over the last six months, the average 5 year fixed posted mortgage rate has also remained unchanged. These rates are impacted by bond yield and lender pricing, not the overnight rate. While there are lots of different terms for fixed mortgages, the 5 year term remains very common, and the posted mortgage rate for that term has stayed constant at 6.09% since October, 2025.

The posted mortgage rate is different than the discounted rate that lenders actually offer, currently around 3.69% to 4.09%, but in general fixed mortgage rates have remained relatively unchanged, just like the variable rate.

To summarize, the cost of borrowing in the last six months has basically remained the same, and the next couple of months will likely see that continue.

On the variable rate side, the BOC announcement a couple of days ago that kept the overnight rate at the same 2.25% we’ve had over the past six months means variable rates will not move over the next six to eight weeks. For fixed rate mortgages, the forecast for bond yields is mostly flat, with perhaps a slight increase, so those mortgages will also likely not change much through May and June.

If the cost of borrowing has been steady for the past six months, with it likely to remain unchanged for the next couple of months, then why are buyers holding off?

Factor Number Two – Prices

If we’re clear that buyers are not holding off on their purchase decision because it’s getting more expensive to finance homes, or because they are worried it will get more expensive shortly, is it because of the price of real estate?

While no one would argue that our real estate is inexpensive, it’s been costly for a long time now. Perhaps it’s because prices are rising, so despite the same interest rates for mortgages, the size of the mortgage – and the cost to carry it – are preventing buyers from jumping into the market.

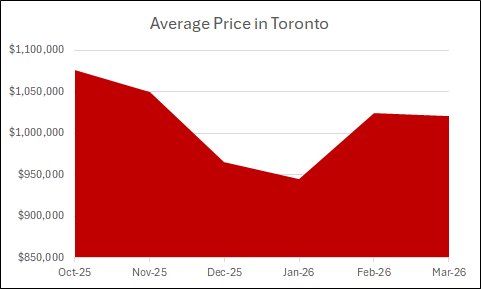

Here’s the average price for real estate in Toronto from October 2025 to March 2026. We don’t have the April data yet, but it hasn’t skyrocketed.

You can see that in the six months of data here, the average price dropped in November, December, January and March, with an increase in February. In October 2025, the average price in the city was $1.076M, and as of the end of March 2026, it was $1.02M. That’s about a $56,000 drop, so on average, it actually costs less to buy now than it did six months ago. With borrowing costs remaining the same, the cost of your mortgage payment is down on average, because you have a lower mortgage due to the lower purchase price.

If buyers were holding off because they saw the market crashing, with lower prices every month, it would make sense. After all, no one wants to purchase an asset that is worth less and less as time goes on. The past six months saw a typical seasonal change, with the holidays and dead of winter seeing lower average prices before a slight, but temporary bump as we headed into spring. The drop from October to March of $56K is about a 5% difference from high to low, and that’s a far cry from a market crash.

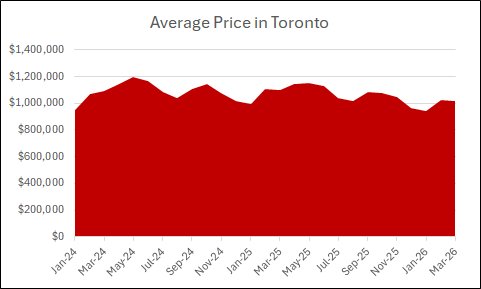

Here’s a chart that shows the average price in Toronto for all of 2024, 2025 and the first quarter of 2026. A lot of fluctuations, but absolutely not a crashing market. In fact, if we compare the price at the end of March 2026, which was $1.02M, with the price at the start of January 2024, which was $952K, Toronto’s market has risen 7% in the past two years and a bit.

If you’re looking at the chart and you’ve been waiting for a significant drop in average prices so you can buy, you’ll view it as a reason to keep waiting. In the same vein, if you’re hoping to buy real estate to see it increase in value significantly over time, the chart says there is no rush for you to jump into the market. Both of those interpretations speak to the public perception of the real estate market, which is the third factor influencing buyer decisions.

Point The Third – Perception

If the cost of borrowing has remained unchanged in the past six months, and the cost of real estate has dropped by over $50K on average – but with no consistent trend or market crash – why are buyers waiting?

Our answer is that the perception of the value of owning real estate in Toronto and the GTA has fundamentally shifted in last five years. Prior to COVID and the turmoil of our recent economic, military and climate challenges, the way we viewed real estate was significantly different than it is now.

After years of consistent price appreciation in the 2000s and beyond, there was a perception amongst the general public that real estate always goes up. With such a belief in place, as well as historically low interest rates and a healthy economy, buyers seized the opportunity to make a purchase.

If the general consensus was real estate always goes up, the rude awakening of the past couple of years has resulted in a new, equally inaccurate consensus, which is that real estate is never going to go up again. There are some people who believe Toronto and GTA real estate markets will experience a significant crash in the near future, but that has always been the case. The more impactful shift in belief that is impacting our level of sales is that a significant amount of people believe that real estate won’t ever go up in value.

The effect of this belief is a lack of urgency, as there is no rush to buy a property when prices will be the same – or perhaps even lower – in a week, a month, or a year from now. In a way, the lack of change in the cost of borrowing reinforces this belief, as it definitely isn’t getting more expensive to finance your purchase. With no absolute end in sight to the current level of interest rates being offered, it is like a sale at a store that seems to be perpetual. If you can’t get to the store this week, or next week, don’t stress about it because the same sale prices will be there whenever you get around to it.

Perception does shift over time and in many ways it is the most impactful of the three factors that influence when a buyer decides to make a move. The cost of borrowing and the price of real estate influence that perception, but if we’re experiencing a time of scarcity and economic uncertainty, buyers are fearful of making a move at the wrong time.

As long as we have significant uncertainty about what is coming next, how our economy will fare and whether our jobs are secure, major decisions will be difficult to make. Given the still lofty heights of the price of real estate in Toronto and the GTA, that means buyers will remain on the fence until a clear picture of what’s coming next is revealed.

The people who are buying and selling in these uncertain times are doing so because they have to make a move, not because the timing is ideal. If you are one of those people, who don’t have the luxury of waiting until you know for sure what’s coming next, then you need a real estate agent who understands the market and how to get you the best possible result. Get in touch with us to talk about the next steps!