Every couple of years we seem to see Toronto increasing their municipal land transfer tax (LTT) on luxury properties. It happened back in 2024, when increased rates were imposed upon sales in Toronto of properties over $3M, and it’s just happened again.

As of April 1, 2026, we have new rates for the LTT on the sale of properties over $3M in Toronto. The provincial land transfer tax has not made any similar changes at any point, but the city of Toronto is rapidly increasing the cost to buy within the Toronto boundaries.

We looked at the anticipated increased revenue the city would make when they did this back at the start of 2024, we said they’d bring in about $27M in additional revenue as a result of the increases. That sounds like a pretty significant amount, but keep in mind that back in late 2023, the City of Toronto’s updated Long Term Financial Plan and staff report showed an estimated $1.5 billion starting pressure for the 2024 operating budget and $29.5 billion in capital needs, which both form part of a $46.5 billion shortfall over the next 10 years. The forecasted $27M would have brought in less than 2% of the amount needed to address the operating budget shortfall.

Given the city remains in difficult financial circumstances, it is clear that the increased tax didn’t help in a material fashion. The latest increase is actually going to be far less impactful, as it is mostly increases of around 1% for those higher price bands.

Let’s look at the new changes and how much additional money it could bring in – plus how many deals need to be lost as buyers decide to purchase their high end homes outside of the city.

Apples to apples.

We’re primarily focused on resale properties in our team and the data we can access is largely limited to residential resale properties. As such, all of our analyses below are based on that data. We’re after some broad (but accurate) implications of the new LTT rates, but we aren’t considering:

- non-MLS transactions

- builder/direct new-home and new-condo closings

- commercial / industrial / multi-residential / vacant land transfers

- other taxable conveyances the City records but that do not show up in our records

While some of the specific numbers of the implications of the new LTT rates will be understated, our analysis does paint a clear picture of what it means to the resale market. Now that we’re officially covered, let’s get into it.

First, a history lesson.

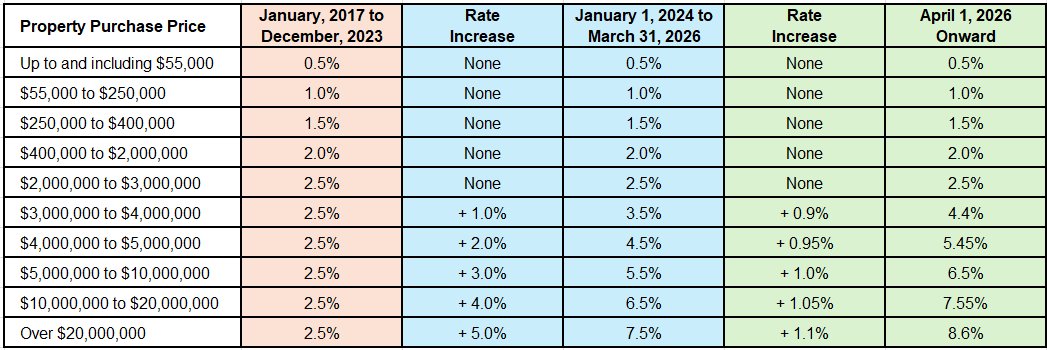

We’ve created a handy chart to show the recent history of the Toronto Land Transfer Tax. The orange column is what it was for about six years, and the blue columns show the rate increase amount that was put into place as of January 1, 2024. The green column is the brand new rate increase amounts that apply to properties bought in the city as of April 1, 2026.

There have been no changes made to the land transfer tax due on the purchase of any properties up to $3M, but if you’re at that level or higher, we saw it go from a flat rate of 2.5% on any amount above the $3M level, to a graduated system. The higher the price point, the higher the rate you’re paying on that portion of your purchase.

The latest round of increases have added about 1% to most of the price bands, with a range from 0.9% to up to 1.1%.

It’s all marginal.

A reminder that the land transfer tax is a marginal tax bracket, which means that for any price above a threshold, you pay:

- The full tax from all lower brackets

- Plus the tax on the portion that falls inside the current bracket

For example, a $1.2 million purchase does not pay 2.0% on the full $1.2 million. Instead, it pays:

- 5% on the first $55,000 = $275

- 0% on the next $195,000 = $1,950

- 5% on the next $150,000 = $2,250

- 0% on the remaining $800,000 = $16,000

- Which would bring the total municipal land transfer tax to $20,475.

This is relevant as we look at what impact these higher tax brackets will have on the sales taking place moving forward.

The past ain’t the future.

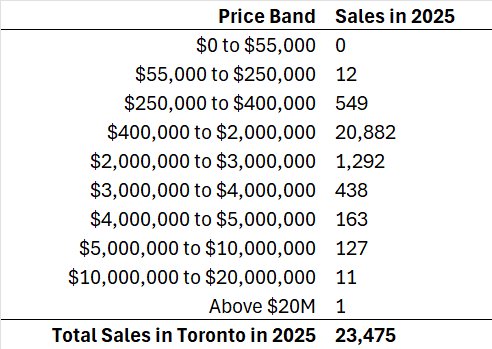

A caveat we often give is that what happened in the past is not necessarily indicative of what will happen in the future. That being said, we need to base our analysis on certain assumptions, so the big assumption in our analysis here is that we’ll see similar types of transactions and numbers of transactions in 2026 as we did in 2025. Here’s how the 23,475 sales in the city of Toronto were spread across the various price bands.

A few things about the above data are very relevant to our review.

First, 97% of the sales that took place in Toronto in 2025 were under $3M, which means the change that just took place is utterly irrelevant to those sales. The Toronto LTT rate for these properties has not changed since 2017 and they can go merrily about their business.

The next thing worth pointing out is that the 740 sales that were in the $3M plus price bands last year were mostly in the $3M to $5M range. 59% of the sales were in the $3M to $4M band and another 22% were in the $4M to $5M band, so over 80% of the sales were in that $3M to $5M range.

If we assume that 2026 will see a similar spread of deals as we saw in 2025, how are these higher land transfer tax rates in those price bands going to bring in to the city in increased revenue?

It’s more, but it’s not a lot more.

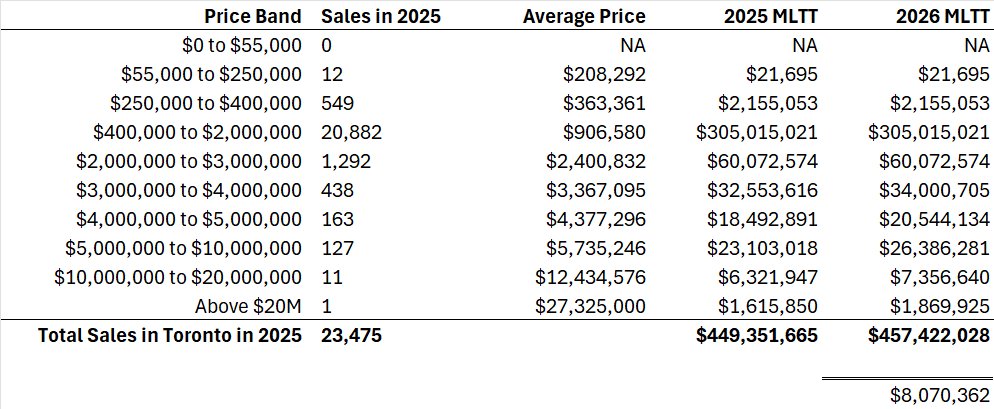

We pulled the average price for each of the price bands for the sales in 2025 and then calculated the Toronto LTT for each of those bands. This is relying on averages within each price band so it will not be 100% accurate, but it is enough to give us an idea of what 2026 will look like for increased revenue with the new increased LTT rates.

The city would have brought in about $450M in municipal land transfer tax in 2025 based on these sales. With the new higher rates for the higher end price points, that means an estimated revenue for 2026 of about $458M, which works out to about $8M more in land transfer tax revenue for the city.

As we see very few sales at the $5M or above price point, the bulk of this $8M comes from sales in the $3M to $5M range.

$8M is still better than a kick in the pants, right?

The final aspect of the new LTT tax rates worth discussing is the fact that our model makes the assumption that the same level of sales take place in Toronto despite increasing costs for those buyers. While it may be unlikely that a lower price point buyer will choose to buy outside of the city to save on the land transfer tax, we have had clients who considered the difference in closing costs significant.

At the higher price points that this latest round of LTT rate increases impacts, the difference between what you pay in Toronto versus surrounding municipalities amounts to significant dollars.

For example, a $5 million buyer in Toronto would pay about $272K in total LTT, of which $112K is the provincial portion. If the buyer chose to purchase instead in another city such as Oakville, they would save $160K on their closing costs. That’s a significant amount of money and while the latest increase in Toronto’s LTT rates doesn’t materially change the amount they pay, it is reaching levels that could result in some buyers deciding they’d rather put that money into a home purchase outside of Toronto.

While it is complicated to project how many lost deals it would take for the city to not see that projected $8M increased LTT from high end sales, we know that any purchase that moves outside of the city loses the entirety of the MLTT, not just the portion at the higher end. Our calculation is that it would take about 67 of these high end deals leaving the city for that projected $8M in extra LTT revenue to disappear completely.

We regularly work with buyers and sellers impacted by decisions like this latest Toronto LTT rate increases, and it’s important that your agent understands the factors that influence the high end and luxury market in the city. If you’re looking to buy or sell in the $3M plus range and want agents that understand how that segment actually works, get in touch!